Why Insurers Prefer Generic Drugs: How Formularies Control Costs and Guide Prescriptions

Most people don’t realize their insurance plan is secretly steering them toward certain pills - not because those pills are better, but because they’re cheaper. That’s the reality of preferred generic lists, the hidden engine behind how health insurers manage billions in drug spending every year. These aren’t random choices. They’re carefully built systems designed to save money without sacrificing safety. And if you’re taking any regular medication, understanding how they work could save you hundreds - even thousands - a year.

How Formularies Work: The Tiered System You’re Already On

Every health insurance plan, whether it’s Medicare, Medicaid, or a plan from your employer, uses a formulary - a list of approved drugs. But it’s not just a list. It’s a tiered ranking system. Think of it like a loyalty program, but for pills. Tier 1 is where the magic happens. This is where preferred generics live. These are exact copies of brand-name drugs, approved by the FDA, with the same active ingredients, same dosage, same effect. But they cost 80-85% less. For example, the brand-name cholesterol drug Lipitor might cost $300 a month. Its generic version, atorvastatin, costs $12. That’s not a typo. Tier 2 includes brand-name drugs that insurers still cover, but at a higher cost to you. Tier 3 is for non-preferred brands - the ones insurers really don’t want you taking unless absolutely necessary. Tier 4? That’s where specialty drugs live: biologics for rheumatoid arthritis, cancer treatments, rare disease therapies. These can cost over $1,000 a month. The numbers don’t lie. In 2023, 98% of commercial insurance plans and 100% of Medicare Part D plans used this tiered structure. And in nearly every case, Tier 1 was reserved for generics. Why? Because the math is irresistible. When a drug has six or more generic competitors, prices can drop by up to 95%. Insurers don’t just encourage generics - they make them the default.Why Insurers Push Generics: It’s All About the Numbers

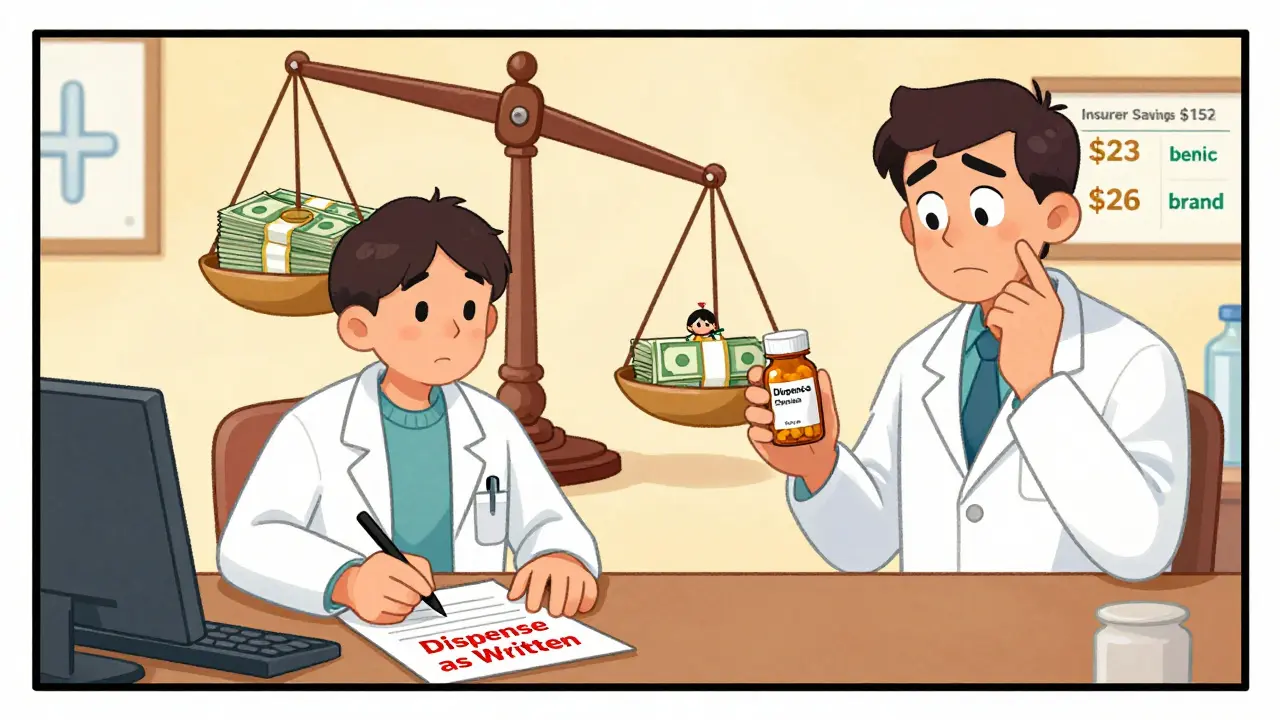

Insurance companies aren’t being charitable. They’re businesses. And their job is to control costs so premiums don’t skyrocket. Generic drugs are the single biggest tool they have to do that. The U.S. generic drug market hit $122.7 billion in 2023. That sounds huge - until you realize it covers 90% of all prescriptions dispensed but only 23% of total drug spending. That’s the power of generics. For every dollar spent on brand-name drugs, insurers spend less than a quarter on generics - and get the same clinical result. Pharmacy Benefit Managers (PBMs) - the middlemen between insurers and drugmakers - are the ones negotiating these deals. They don’t just buy drugs. They bargain. For brand-name drugs, they get rebates of 25-30%. For generics? They lock in bulk discounts so deep that the list price is often lower than what pharmacies pay for the brand version. This isn’t theoretical. In 2022, a Medicare Part D study found that when a brand and generic were in the same tier, the brand’s average list price was $349. The generic? $197. But because most plans use flat copays (not percentage-based coinsurance), the patient paid just $26 for the brand and $23 for the generic. The insurer? They saved $152 per prescription. That’s why insurers don’t just prefer generics - they make them the easiest, cheapest option. And if you don’t choose them? You pay more.

The Catch: When Generics Don’t Work - And Why It Happens

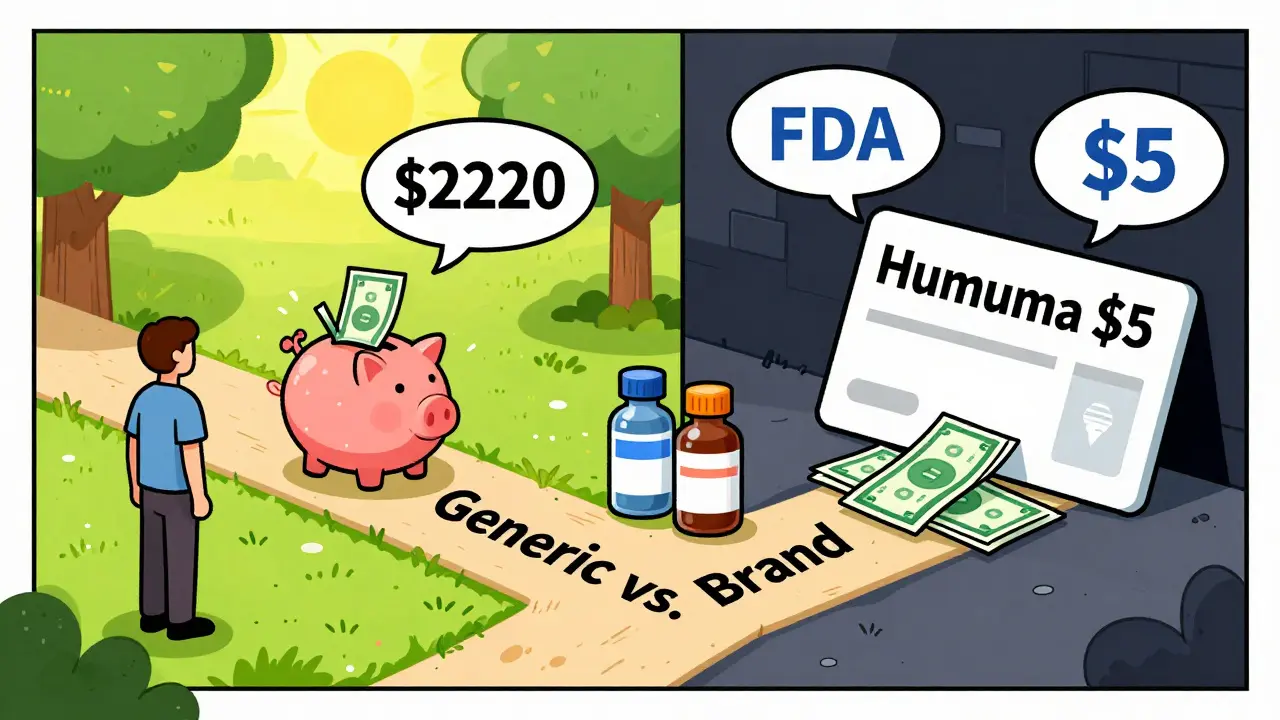

You might think: “If generics are the same, why would anyone take the brand?” The answer isn’t always about effectiveness. Sometimes, it’s about access. Take biosimilars - the generic version of complex biologic drugs like Humira or Enbrel. These are expensive, often over $1,000 a month. Biosimilars like Amjevita or Cimzia can cut that cost by half. But here’s the problem: brand-name manufacturers offer co-pay cards that reduce your out-of-pocket to $5 a month. Biosimilar makers? They don’t. Why? Because they’re new, smaller companies without the same marketing budgets. So even though Amjevita costs $850 a month and Humira costs $1,200, a patient on Humira might pay $5. A patient switched to Amjevita? They pay $850. That’s not savings. That’s a trap. And it’s happening to tens of thousands of people. Then there’s the issue of narrow-therapeutic-index drugs - medications where even tiny differences in dosage can cause serious side effects. Warfarin, used to prevent blood clots, is one. About 23% of doctors refuse to switch patients from brand to generic warfarin, not because generics are unsafe, but because they’ve seen patients struggle with stability after switching. The FDA says generics are bioequivalent within 80-125% of the brand - which is legally safe. But real-world practice doesn’t always match the lab. And then there’s step therapy. Insurers make you try the generic first. If it doesn’t work, you file an appeal. If it’s denied? You wait. A 2022 AMA report found 42% of doctors reported delays in treating chronic pain because patients had to fail on a generic before getting the drug their doctor prescribed.

What You Can Do: Navigate the System Like a Pro

You don’t have to be stuck. You can fight back - and save money doing it. First, check your formulary. Every year during open enrollment, insurers update their lists. Go to your plan’s website. Look for “formulary” or “preferred drug list.” See where your medication sits. If it’s in Tier 3 or 4, ask your pharmacist: “Is there a preferred generic alternative?” Second, ask your doctor to write “dispense as written” on your prescription. In 89% of states, pharmacists can automatically swap a brand for a generic unless the doctor says otherwise. That’s your power. Use it. Third, appeal. If your insurer denies coverage for a brand-name drug your doctor says you need, file an appeal. In 68% of cases, these appeals succeed - especially when your doctor writes a letter explaining why the generic won’t work for you. You don’t need a lawyer. Just a clear note from your provider. Fourth, use GoodRx or SingleCare. These apps show you cash prices at local pharmacies. Sometimes, paying cash for a generic is cheaper than your copay. Especially if you’re on a high-deductible plan. Finally, track your savings. One Reddit user switched from brand-name levothyroxine to generic and dropped from $187 to $12 a month. That’s $2,220 saved a year. That’s not luck. That’s strategy.The Future: Where Formularies Are Headed

The system isn’t static. It’s changing fast. Starting in 2025, Medicare will require all Part D plans to place biosimilars in the same tier as their brand-name counterparts. That’s huge. It means patients won’t be penalized financially for choosing the cheaper option. Experts predict this will boost biosimilar use from 15% to 45% in just a few years. Meanwhile, UnitedHealthcare and others are testing “value-based formularies.” These don’t just look at price. They look at real-world outcomes. Does this drug actually keep patients out of the hospital? Does it reduce ER visits? If yes - it moves up the tiers, even if it’s expensive. But there’s a dark side: accumulator adjuster programs. These let insurers count your manufacturer co-pay cards toward your drug costs - but not toward your out-of-pocket maximum. So you’re paying $5 a month for your drug, but your deductible keeps climbing. That’s a loophole. And it’s spreading. The bottom line? Preferred generic lists aren’t going away. They’re getting smarter. And if you understand how they work, you can turn them from a barrier into a tool - one that saves you money, keeps you healthy, and gives you more control over your care.Why do insurance companies prefer generic drugs over brand-name ones?

Insurance companies prefer generic drugs because they’re clinically equivalent to brand-name drugs but cost 80-85% less. For example, a brand-name statin might cost $300 a month, while its generic version costs $12. With millions of prescriptions filled each year, this saves insurers billions. Pharmacy Benefit Managers (PBMs) negotiate bulk discounts on generics, making them the most cost-effective option. This lowers premiums for everyone and reduces overall healthcare spending.

What’s the difference between Tier 1 and Tier 2 drugs on a formulary?

Tier 1 includes preferred generic drugs with the lowest out-of-pocket costs - usually $5 to $15 for a 30-day supply. Tier 2 includes preferred brand-name drugs and some higher-cost generics, with copays typically between $25 and $50. The main difference is price: Tier 1 is the cheapest option insurers encourage you to use. Tier 2 is still covered, but you pay more. Insurers design these tiers to steer patients toward lower-cost alternatives without denying access to necessary medications.

Can I still get my brand-name drug if it’s not on the preferred list?

Yes, but it’s harder. If your drug is in Tier 3 or 4, you’ll pay significantly more - often $50 to $100 or more per prescription. You can ask your doctor to file a prior authorization or appeal, explaining why the generic won’t work for you. About 68% of these appeals are approved when supported by medical documentation. You can also pay cash using apps like GoodRx, which sometimes offer lower prices than your insurance copay.

Why are biosimilars cheaper but sometimes cost me more out-of-pocket?

Biosimilars are cheaper for insurers - but brand-name biologic manufacturers offer co-pay cards that reduce your monthly cost to as low as $5. Biosimilar makers rarely offer these because they’re newer and have less marketing budget. So even though a biosimilar like Amjevita costs $850 a month versus $1,200 for Humira, you might pay $5 for Humira and $850 for Amjevita. That’s why some patients end up paying more, even though the drug is technically cheaper. This is a major flaw in how formularies handle biologics.

How often should I check my insurance’s drug list?

You should check your formulary every year during open enrollment, which usually runs from October to December. Insurers change their preferred lists annually - sometimes removing drugs, moving them to higher tiers, or adding new generics. A 2022 CMS study found patients who reviewed their formulary saved an average of $417 per medication per year. Even a small change - like a drug moving from Tier 2 to Tier 3 - can add $100+ to your monthly cost.

Do pharmacists automatically switch my brand-name drug to a generic?

In 89% of U.S. states, pharmacists can substitute a brand-name drug with a generic unless your doctor writes “dispense as written” on the prescription. But 37% of patients don’t know this. If you want to stay on the brand, ask your doctor to add that note. If you’re okay with the generic, let the pharmacist switch it - you’ll save money without any loss in effectiveness. The FDA confirms generics meet the same safety and quality standards as brands.

15 Comments

Mussin Machhour

Just switched my levothyroxine to generic last month and saved $200 a month. My pharmacist didn’t even ask - just swapped it. I was nervous at first but felt zero difference. If you’re paying full price for brand-name stuff, you’re literally throwing money away. This system isn’t evil - it’s just rigged to make you think it is.

Linda B.

Let me guess - the FDA is in cahoots with Big Pharma and PBMs to keep you docile while they drain your bank account with fake generics that contain fillers from China that slowly destroy your liver. They call it ‘bioequivalent’ but what they really mean is ‘close enough so you don’t sue us.’ You think you’re saving money? You’re just becoming a lab rat in their profit-driven experiment.

Christopher King

Think about this - formularies are the silent dictatorship of the pharmaceutical-industrial complex. They don’t care if you live or die - they care if your copay is under $25. The fact that a $12 pill can replace a $300 one isn’t progress - it’s dehumanization. We’ve turned medicine into a spreadsheet. And now they want us to cheer because we’re getting the discount version of our survival.

They call it ‘cost-effective.’ I call it ‘soul-crushing.’

Bailey Adkison

Generic drugs are not the same as brand name. The FDA allows up to 20% variation in bioavailability. That’s not equivalent. That’s statistically significant. And yet doctors and insurers pretend it’s a nonissue. You’re not saving money - you’re gambling with your health. And if you’re okay with that, fine. But don’t pretend it’s science.

Michael Dillon

My mom’s on warfarin. Doctor refused to switch her to generic. Said she’d bleed out. She’s been stable on brand for 12 years. I get the math but real people aren’t data points. Some of us need the brand. And if your insurer won’t cover it unless you prove you’re dying? That’s not a system. That’s a trap.

Gary Hartung

Oh, so now we’re supposed to be grateful that our lives are being optimized by corporate algorithms? The fact that a $12 pill is ‘just as good’ as a $300 one is a tragedy - not a triumph. We’ve reduced human health to a commodity, and now we’re being told to applaud the discount. What’s next? Generic oxygen?

And don’t even get me started on the co-pay cards. That’s not healthcare. That’s psychological manipulation disguised as charity.

Oluwatosin Ayodele

In Nigeria, we don’t have formularies. We have pharmacies that sell whatever the distributor brings. Sometimes the pills are fake. Sometimes they’re expired. Sometimes they’re from India and labeled in Mandarin. You think your $12 generic is bad? Try getting any pill at all without a doctor’s note and a prayer. Your system is broken but at least it’s organized.

Carlos Narvaez

Formularies aren’t the enemy. The lack of transparency is. If insurers published real-time pricing data - not just copays but what they actually pay - we could see the true cost. Until then, we’re all just guessing.

Harbans Singh

My cousin in India takes the same generic as I do - made in the same factory. She pays $0.50. I pay $12. Why? Because of insurance bureaucracy. We’re not saving money - we’re paying for middlemen. The real solution isn’t more generics. It’s removing the middlemen entirely.

Justin James

Here’s the real story no one tells you: PBMs don’t just negotiate discounts - they take kickbacks from drugmakers to put their brand-name drugs on higher tiers. That’s why some generics are ‘preferred’ and others aren’t. It’s not about cost. It’s about who paid the most. The whole system is a shell game. You think you’re getting a deal? You’re just the sucker holding the empty cup while the house wins every time.

And don’t even mention GoodRx - those apps are owned by the same companies that run the PBMs. You’re not comparing prices. You’re being funneled into their ecosystem. They want you to think you’re fighting the system. You’re just dancing on their stage.

Every time you use a co-pay card, you’re helping them hide the true cost from Medicare. That’s why your premiums keep rising. You’re not saving money. You’re subsidizing the fraud.

They say generics are safe. But the same company that makes the brand also makes the generic. Same factory. Same batch numbers. Just a different label. So why does the brand cost 25 times more? Because they can. And you’re letting them.

And now they’re pushing biosimilars - which are just as expensive to make - but they’ll make you pay full price because they don’t have the marketing budget. But the brand? They’ll give you a $5 card. That’s not competition. That’s extortion.

They’re not trying to save you money. They’re trying to make you think you’re saving money so you don’t ask why your insurance premium went up 17% last year while your copay stayed the same. Wake up. This isn’t healthcare. It’s a Ponzi scheme with pills.

Zabihullah Saleh

Back home in Afghanistan, we used to trade medicine like currency. A bottle of antibiotics could buy a week’s food. Now I live in America and I’m told I’m lucky because my $12 pill is ‘affordable.’ But I still feel the same fear - that tomorrow, the pill won’t be there. Maybe the system is different here. But the anxiety? That’s universal.

Winni Victor

Ugh I hate this so much. Like yeah I saved $2000 but now I feel like a corporate puppet who traded dignity for a discount. I’m not a spreadsheet. I’m a person who just wants to not feel like I’m being gaslit by my own insurance company every time I fill a prescription.

Rick Kimberly

While the economic rationale for formulary tiering is sound, the ethical implications warrant deeper scrutiny. The commodification of therapeutic outcomes risks undermining the physician-patient relationship and eroding trust in clinical autonomy. A system that prioritizes cost efficiency over individualized care may yield short-term fiscal gains but at the expense of long-term health equity.

Terry Free

Generic? More like generic lie. They’re not the same. And the fact that you’re okay with it means you’ve given up. Welcome to healthcare in 2025 - where your life is priced in cents and your dignity is a deductible.

Lindsay Hensel

Thank you for writing this. I’ve been fighting my insurer for 8 months to cover my brand-name drug. My doctor’s letter worked. But I cried the whole time. No one should have to beg for basic health. This system breaks people. And I’m so tired.

Recent Posts

-

Diphenhydramine Overdose: Recognizing Antihistamine Toxicity and Emergency Care

-

How to Get Prescription Assistance Programs from Manufacturers

-

Triple-Negative Breast Cancer Treatment: New Strategies and Clinical Trials

-

Managing Dry Mouth from Medications: Causes, Risks, and Relief

-

Citalopram vs Escitalopram: Managing QT Prolongation and Dose Limits

Write a comment